Multifamily Market Update: Early Signs of Recovery

Cap Rates Showing First Signs of Compression

CBRE’s latest U.S. Cap Rate Survey (H1 2025) just dropped, and the numbers are telling. Over 200 professionals across 50+ markets contributed more than 3,600 cap rate estimates, and the trend is clear:

All-property cap rates fell ~9 bps in the first five months of the year.

The movement is small—but important. It may signal we’ve already hit the peak and are now entering the early stages of cap rate compression.

Encouragingly, almost every property type shifted in the same direction, showing broad alignment across the market.

Why this matters: With the 10-year Treasury swinging between 4.8% and 4.2% this year, even a small cap-rate dip in such a volatile environment is meaningful. Investors are beginning to price in less risk—and that’s good news for multifamily.

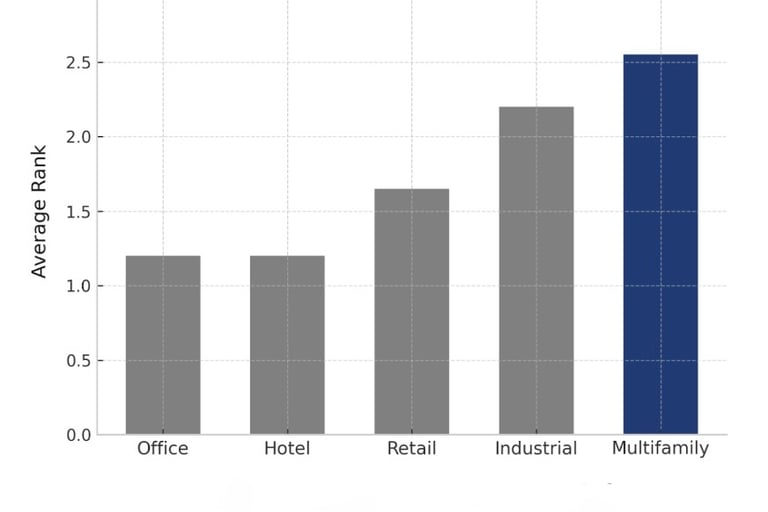

Respondent average rank of each sector in order of greatest to worst investment performance

during the next 10 years (5 = Greatest expected performance)

When asked which sectors will perform best in the months ahead, survey respondents ranked multifamily as #1—edging out industrial. Why?

Strong renter demand continues to absorb supply.

Vacancies are stabilizing, with the national average projected to end 2025 at 4.9%.

Annual rent growth is expected at 2.6% nationally, with stronger growth in select regions.

Supply Wave Peaking, Recovery Kicking In

We’re still working through the biggest apartment construction boom since the 1970s, but the good news is that much of the new supply is peaking right now. Ten of the sixteen busiest development markets have already passed their peak, and the rest will hit theirs in 2025.

By mid-next year, new construction starts are expected to be way down—about 74% lower than the 2021 peak. With fewer new projects coming online, renter demand will start catching up, vacancies will fall, and rent growth will pick up again heading into 2026.

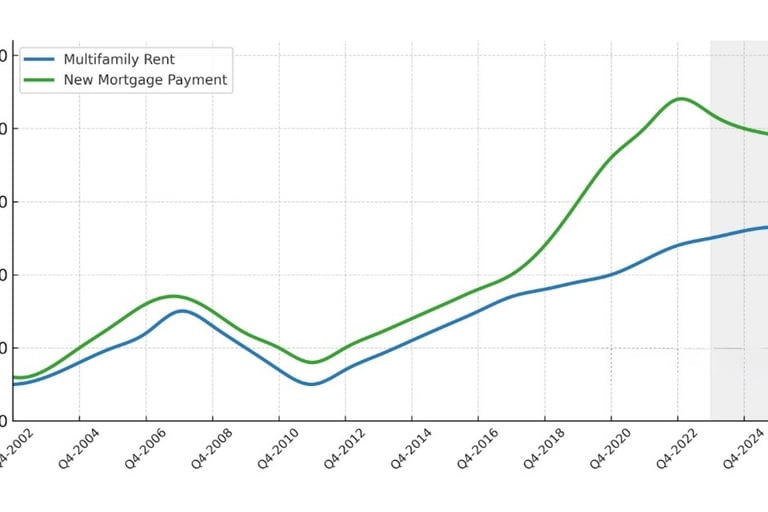

Here’s another reason multifamily looks strong: buying a home is still much more expensive than renting. Right now, the average monthly mortgage payment is about 35% higher than rent. Even as that gap shrinks a bit, it’s still enough to keep many families renting.

On top of that, most current homeowners have locked in mortgage rates below 5%. They don’t want to sell, which keeps inventory tight and home prices high. All of this means demand for rentals will stay strong well into the future.

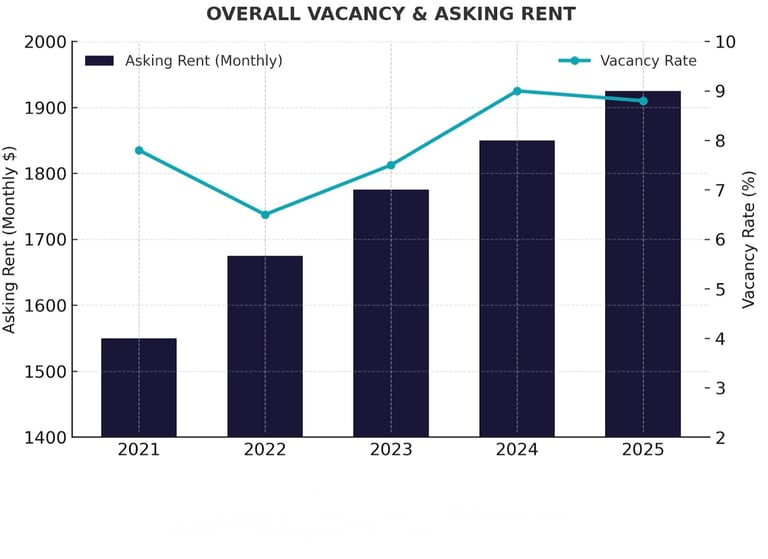

Vacancy Improvement Continues in Q2 2025

For the second quarter in a row, more apartments were rented than new ones built. That’s a big deal because it’s the first time since 2021 that vacancies (empty units) have consistently gone down.

That said, the overall vacancy rate is still about 2% higher than the long-term average of 7%, so the market isn’t fully balanced yet. If we look only at buildings that are already stabilized (not brand-new ones still leasing up), vacancies are closer—just 0.6% above normal levels.

The demand for apartments in Q2 was strong—actually one of the top six quarters since 2000. But there’s a small catch: when we adjust for the usual seasonal bump in spring, demand wasn’t quite as strong as it typically is. Normally, second-quarter leasing activity is about 30% higher than the first quarter, but this year it was only about half of that.

This slowdown could be tied to lower consumer confidence. Surveys from both the University of Michigan and the Conference Board showed sharp drops in how people feel about the economy, with UMich hitting its second-lowest reading ever in April and May.

Bottom line: Vacancies are improving, and demand is still solid, but early signs suggest renters might be feeling more cautious. This is something to keep an eye on as we move through the rest of the year.

Regional Highlights

Sun Belt & Mountain West: Short-term pressure from high supply, but fundamentals improve as completions slow.

Midwest, Northeast & Gateways: Lower exposure to new supply means rent growth >3% in 2025, outperforming national averages.

High-growth markets (Phoenix, Salt Lake City, Nashville): Expect premium compression as supply shrinks and renter demand accelerates.

What This Means for Investors

Cap rates appear to be turning the corner.

Multifamily fundamentals remain strong despite supply headwinds.

Renters will continue choosing apartments over costly homeownership.

Markets with big pipelines are on the verge of recovery, while stable markets will outperform in the near term.

Let’s Build Wealth Together

If you want to learn how to take advantage of these shifts,

→ Schedule a Discovery Call here

Win Big, Win Together,

The Trinity Commercial Partners Team

Christian Marcantonio

Mysti Marcantonio

Angela Neal

Managing Partner

Managing Partner

Managing Partner

The information contained on this website is for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities. Investments offered by TrinityCommercialPartners.com, LLC are made pursuant to Rule 506 of Regulation D and Regulation A under the Securities Act of 1933 and are available only to qualified investors. Investments under Rule 506(c) are limited to accredited investors as defined by the SEC, while Regulation A offerings may be available to both accredited and non-accredited investors subject to specific terms.

Investing in private real estate securities involves significant risks, including the potential loss of principal, lack of liquidity, and no guarantee of returns. Past performance is not indicative of future results. Any forward-looking statements or projections are based on assumptions that may change, and actual results may differ materially.

Investors should conduct their own due diligence and consult with their financial, tax, and legal advisors before making any investment decisions. Nothing on this website constitutes tax, legal, or investment advice.

By accessing this website, you acknowledge and agree to the terms of this disclaimer.

Head Office

Jacksonville, FL 32246

© 2025 by Trinity Commercial Partners LLC

Other Links

Navigation

Investor Login